Financial Services

Investment Advisors: Get Ready for

State Regulation of Social Media

Although the author of this post is an attorney, nothing contained in this post should be considered legal advice. For legal questions, please consult with an attorney from your jurisdiction.

State Regulation of Social Media

Although the author of this post is an attorney, nothing contained in this post should be considered legal advice. For legal questions, please consult with an attorney from your jurisdiction.

{kind=link}

In a bold move, the Securities Division for the Commonwealth of Massachusetts announced guidelines on the use of social media for state investment advisors who were previously permitted to market their services on social networks, such as LinkedIn, Twitter and Facebook, without social media guidelines. Coming just two weeks after the SEC issued its own set of social media guidelines, the Division's actions have raised the bar for other states to take similar action for the protection of investors.

Though many investors think that all investment advisors are regulated by the SEC, the reality is that the SEC only regulates investment advisors who manage $25 million or more in client assets. For investment advisors managing less the $25 million in client assets, the responsibility of regulation is left to the securities regulator for the state where the adviser has its principal place of business.

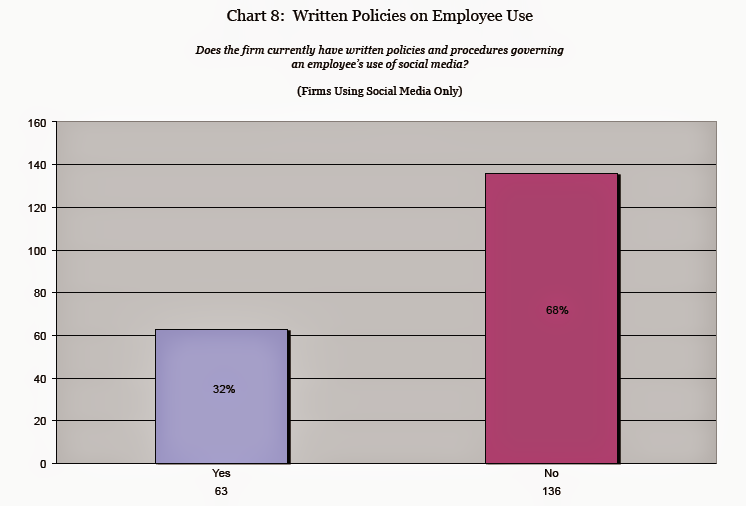

In July of 2011, the Massachusetts Division conducted a survey of investment advisers registered and doing business within the Commonwealth to "to determine the scope of investment advisers' use of social media, and what, if any, record retention and supervisory procedures have been implemented or utilized by those advisers." Seven-nine percent of the 576 investment advisers registered with the Division responded to the survey.

State Investment Advisors Lack a Social Media Policy & Fail to Monitor Advisor Social Media Activity

A report of the Division's survey results revealed that sixty-eight percent of investment firms using social media failed to have written policies on employee use of social media and that fifty-seven percent failed to retain records of content shared on social networks.

Though many investors think that all investment advisors are regulated by the SEC, the reality is that the SEC only regulates investment advisors who manage $25 million or more in client assets. For investment advisors managing less the $25 million in client assets, the responsibility of regulation is left to the securities regulator for the state where the adviser has its principal place of business.

In July of 2011, the Massachusetts Division conducted a survey of investment advisers registered and doing business within the Commonwealth to "to determine the scope of investment advisers' use of social media, and what, if any, record retention and supervisory procedures have been implemented or utilized by those advisers." Seven-nine percent of the 576 investment advisers registered with the Division responded to the survey.

State Investment Advisors Lack a Social Media Policy & Fail to Monitor Advisor Social Media Activity

A report of the Division's survey results revealed that sixty-eight percent of investment firms using social media failed to have written policies on employee use of social media and that fifty-seven percent failed to retain records of content shared on social networks.

{kind=link}

Based on the survey's findings on the failings of self-regulation, namely, the absence of in-house guidelines, archiving and supervision, the Massachusetts Division decided that it needed to provide social media guidelines for investment advisors it is charged with regulating. Massachusetts' decision to issue social media guidelines raises the bar for other states that have yet to issue any guidelines.

Because of Massachusetts' leadership, another stretch of the "Wild West" of social media may be soon coming to a close as other states, invariably, come to recognize that the absence of social media guidelines for a large swath of investment advisors in the social media space potentially puts at risk scores of family life savings and retirement funds. Establishing social media guidelines should help the vast majority of ethical advisors who may have shied away from social media participation due to the lack of guidelines. They should also help trigger earlier detection of unscrupulous advisor activity in the social media space.

Massachusetts Securities Division Confronts the Realities and Detail of Social Media

One of the most intractable, regulatory issues in social media for highly-regulated industries has been "What to do about the sharing of links?" In the pharmacuetical space, the requirement of "fair balance" and other considerations have placed serious constraints on link sharing. For the Massachuesetts Securities Division, however, this issue is not so intractable. Simply, the Division has warned advisors that the sharing of a link, or "retweet" in Twitter, "without context", could well trigger impermissible "adoption" or "entanglement" -- but the key point to observe is that by providing "context", a violation might well be avoided. Though the message is still one of "proceed with caution", it also demonstrates a real understanding of how social media works and how it can be used in a compliant fashion.

Some Key Takeaways and Social Media Best Practices for Massachuesetts Investment Advisors

- As a general rule, social media accounts created or maintained for business will be considered advertising, and subject to the same regulatory requirements as other forms of advertising.

- Advisors are now required to retain records of their social media "advertising" and "correspondence".

- An adviser may also be responsible for content it did not author, i.e., third-party content, if the adviser has some responsibility for its creation (entanglement) or has somehow endorsed it (adoption) after the content was created.

- "Retweets" on Twitter or link-sharing, without "context", may trigger impermissible adoption or entanglement.

- Selectively deleting third-party material unfavorable to the adviser but continuing to display favorable content, may be deemed to adopt the remaining content.

- Advisers should develop policies and procedures that maintain a schedule for review of third party posted content and, if the adviser chooses to remove content, criteria for removal.

- LinkedIn recommendations may constitute impermissible testimonials and advisers should consider a policy to restrict the public posting of client recommendations to their LinkedIn profile.

- Facebook “Likes” by themselves are not likely to give rise to a violation of the prohibition of testimonials, though advisors are warning against entangling themselves in such "Likes". (The Division explained: An adviser that suggests on their webpage that the number of “Likes” received is evidence of their ability as an investment adviser may run afoul of securities laws.)

- Certain social media websites, such as Twitter, may be an inappropriate medium for discussion of performance advertising because of challenges to full and fair disclosure of all material information.

- An adviser should conduct a daily review its social media presence and ensure that any content that could be considered non-compliant is removed or hidden from view promptly.

- To avoid impermissible "adoption" or "entanglement" with third party content, advisors not solicit third party content on their website nor link to third party content that they have not thoroughly reviewed.

- Advisors should provide a disclosure statement on their social media sites.

- On the subject of advisor supervision and compliance, the Division largely embraced and adopted the recently enunciated SEC guidelines, charging its advisors to adhere to those standards, calling upon investment firms to establish a social media compliance program that would specifically address several factors: 1) usage guidelines as to proper and improper use of social media by investment adviser representatives, 2) content standards, 3) the manner and frequency with which an adviser will monitor social media websites, 4) whether investment adviser representatives must have social media content approved prior to public posting, 5) criteria for determining which social media or networking websites may be used by the firm and its representatives, 6) whether to train investment adviser representatives on compliant use of social media, and 7) certification requirements.

- World's Largest Brokerage OKs

Social Networking by Financial Advisors

{kind=link}

Memo heralds new media breakthrough

New York-based financial services powerhouse, Morgan Stanley, the world’s largest brokerage firm, announced, not in a tweet or a blog, but in an old-fashioned, internal memo, plans to “begin a staged, roll-out for Advisors to use Social Media.”

New York-based financial services powerhouse, Morgan Stanley, the world’s largest brokerage firm, announced, not in a tweet or a blog, but in an old-fashioned, internal memo, plans to “begin a staged, roll-out for Advisors to use Social Media.”

Mincing no words about the implications of the announcement, the memo’s author, Andy Saperstein, who heads the brokerage’s U.S. operations, observed:

"This will be a significant competitive advantage."

Morgan Stanley’s decision to invest in social media by allowing, initially, a select group of about 600 of its financial advisors to use social media, will undoubtedly leave others in the highly-regulated financial services sector scrambling to follow the leader.

Regulatory Authority Guidelines Met with Industry Social Media Paralysis

Although the Financial Industry Regulatory Authority (FINRA) had provided the financial services industry with social media guidelines in January of 2010, the highly-regulated financial services sector largely greeted the Authority's invitation to participate in social media with paralysis. Responding, nonetheless, to a keen, continued interest in social media by brokerages, FINRA even provided a session on social media compliance at its 2011 annual conference.

Technology Aids Compliance, Spurs Social Media Participation

A requirement of FINRA's guidelines is the archiving of social media communications, a particularly challenging compliance mandate. To this requirement, Saperstein noted in his memo that:

In the coming weeks, Morgan Stanley will implement a technology solution that will capture and retain all communications on approved social networking sites to comply with regulatory requirements.

Although various archiving vendors exist, Saperstein's memo suggests a "technological solution" that may well be proprietary in nature. Whatever it is, it will be closely scrutinized as an industry standard.

Limited Launch in Late June; Full Roll Out Within 6 Month

{kind=link}

Announcing a tight timeline, Saperstein explained that the first 600 advisors would begin their social media participation in late June, "with access to LinkedIn and partial use of Twitter", with "the rest of the field" having access within six months. (It is worth noting that Morgan Stanley reportedly reaped huge fees from recently underwriting LinkedIn's IPO.)

Firm to Provide Content for Sharing; Participation Preceded by Training and Profile Approval

Saperstein informed employees in his memo that the firm would provide "a tool for Advisors to distribute Firm approved research and content, providing you with a powerful way to share our unique intellectual content with clients and prospects." Providing employees with content to share through social networks to clients and prospects could have a two-fold benefit: it could ensure that the content shared was branded as well as scrutinized for regulatory compliance.

The lucky 600, who will become Morgan Stanley's social media pioneers, were also told that they would receive an e-mail "with more details on training and how to get started by getting your profiles approved."

No Mention of Facebook and Only "partial use of Twitter"

Firm to Provide Content for Sharing; Participation Preceded by Training and Profile Approval

Saperstein informed employees in his memo that the firm would provide "a tool for Advisors to distribute Firm approved research and content, providing you with a powerful way to share our unique intellectual content with clients and prospects." Providing employees with content to share through social networks to clients and prospects could have a two-fold benefit: it could ensure that the content shared was branded as well as scrutinized for regulatory compliance.

The lucky 600, who will become Morgan Stanley's social media pioneers, were also told that they would receive an e-mail "with more details on training and how to get started by getting your profiles approved."

No Mention of Facebook and Only "partial use of Twitter"

Interestingly, the memo makes no mention of the largest social network, Facebook, while stating that the financial advisors "will have access to LinkedIn and partial use of Twitter."

The glaring absence of any mention of Facebook may suggest that that particular social may not be part of the brokerage's initial social media roll out. Like the risk-adverse pharmaceutical sector, another highly-regulated industry, wealth management may yet find too many unresolved compliance issues with Facebook.

Morgan Stanley An Early Student of "Significant Share Gains of Internet Traffic" by Social Networks

In 2008, Morgan Stanley noted the fast-growing role of social media in online communications, outlining "significant share gains of online traffic".

What are your thoughts? Is social media a smart investment for the financial services?

Please make one small investment in social media - join me on Twitter! GlenGilmore

For the text of the Morgan Stanley memo, see: Tweet on the Street

{kind=link}

The glaring absence of any mention of Facebook may suggest that that particular social may not be part of the brokerage's initial social media roll out. Like the risk-adverse pharmaceutical sector, another highly-regulated industry, wealth management may yet find too many unresolved compliance issues with Facebook.

Morgan Stanley An Early Student of "Significant Share Gains of Internet Traffic" by Social Networks

In 2008, Morgan Stanley noted the fast-growing role of social media in online communications, outlining "significant share gains of online traffic".

What are your thoughts? Is social media a smart investment for the financial services?

Please make one small investment in social media - join me on Twitter! GlenGilmore

For the text of the Morgan Stanley memo, see: Tweet on the Street